Sberbank conceived a revolution by identifying telephone fraudsters in real time. And not only Sberbank, Tinkoff Bank too. Probably, the rest will soon catch up. MTS Bank studied the preferences of Russians when paying for goods and services using plastic cards and pay-services, the results are predictable, but the numbers are still interesting.

Have you really taken the scammers seriously?

We are talking about telephone fraud, which we have never really dealt with. Why they did not study seriously, it is understandable, it is a very thankless task. It is difficult and uninteresting for law enforcement to “catch and punish”, the case is slippery, and it is difficult and unproductive to prove anything after an attempt. And after a successful fraud, when the deed is done, the money is stolen and the victim appears, it is not much easier for him that the case was opened. And if brought, then it is almost a notorious “hanging”. Which is not needed by anyone except the victim. It turns out that this area remains out of the spotlight, which certainly makes the scammers really happy.

I advise you to read the full text of the news here, it is really interesting and informative. Quotes:

“Sberbank was the first Russian bank to start detecting telephone fraud in real time, joining forces with telecom operators in a unique technological anti-fraud solution. This solution has no analogues in the world and is being launched jointly with Tele2 and MegaFon, complementing the existing interaction of Sberbank with mobile operators. In the process of connecting – MTS and Beeline.

Now the bank’s anti-fraud system will additionally receive information about fraudulent calls to customers from the anti-fraud platform on the side of telecom operators. This solution allows us to promptly identify fraudulent calls and take measures to protect the bank’s customers. We believe that combining the efforts of the bank’s anti-fraud solutions and telecom operators will increase the efficiency of detecting and preventing telephone fraud. ” Stanislav Kuznetsov, Deputy Chairman of the Management Board of Sberbank.

Stanislav Kuznetsov, Deputy Chairman of the Management Board of Sberbank

It is no secret that Sberbank’s clients are the most affected by fraudsters, for several objective reasons:

- Bank size and popularity. In any case, the number of victims will be greater than that of the peer banks, simply because of the number of clients.

- Targeting scammers. This one directly follows from the first reason, it is logical to focus on the maximum probability of guessing the bank. If the fraudster appears to the victim as a representative of the bank, then the mistake in guessing the name of the bank – consider that 75-80 percent is already a failure of the “mission”. Despite the numerous assurances of pessimists about “leaks of information” and “purchased databases”, the overwhelming majority of such calls are so-called “cold calls”, calls to random phone numbers.

- Fewer scripts, easier to “work”. There is no need to overestimate the intelligence of scammers, there are not so many talented professionals among the dialers, and there are no Wang reading minds at all. Judging by the reviews, most scammers have one scenario and they stupidly follow this scenario. Naturally, this script was written specifically for the owners of Sberbank cards.

- Finally, among the clients of Sberbank there are many elderly people and / or people who are completely unaware of all this. And often gullible people. Sadly, these people are most often the victims of phone calls from scammers.

These are, in fact, only the main reasons why we should be especially pleased with the additional security measures of Sberbank. Here from all sides the stars converge so that even the unhurried gestures of Sber, in terms of money saved from fraudsters, should bring much more benefit than the most modern super-duper protection in a small bank with a couple of hundred depositors. Remember the joke about “The Elusive Joe”? For example, according to the same “Joe model,” no one really needs such investors and can feel relatively safe from fraudsters. But will the small bank survive in the current conditions? This is another question and the very other side of the coin. Finally, the third option is to store money in a glass jar with a tightly screwed lid. The choice, of course, is yours.

Tinkoff writes about the same (probably) in more detail, a couple of quotes:

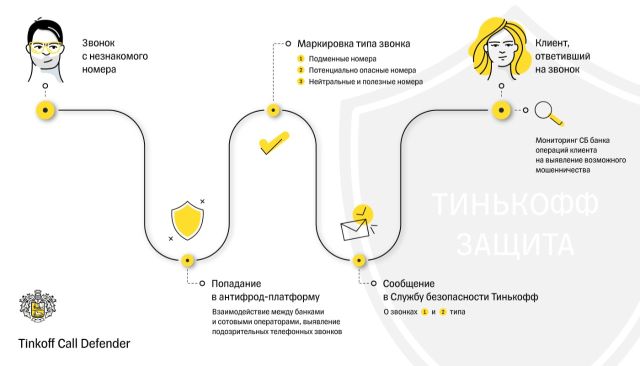

“Tinkoff announces the launch of Tinkoff Call Defender, a platform for preventing fraud using telephone calls, as part of the development of its own customer security system, Tinkoff Zashchita. The platform was developed in partnership with major mobile operators, including Tele2, Megafon, MTS and Tinkoff Mobile.

Tinkoff became the first Russian bank to test and implement into its anti-fraud platform technology developed by the largest mobile operators – Megafon, Tele2, MTS. It is designed to protect customers from the most common method of telephone fraud – social engineering and, in particular, from phone calls with spoofing.

Small offtopic: pay attention to the purposeful use of the name “Sberbank” instead of “Sberbank”. All these zhu-zhu, of course, for a reason, and Sberbank is clearly teaching everyone to call it simply Sberbank, whose sphere of interests is much larger and wider than that of some bank, even if this “some” bank is a whole Sberbank. Will it work? The people are conservative and difficult to retrain.

Now, on the essence of the topic. It seems that they have finally tackled the scammers seriously and at a good technological level. Will this fight be effective? We’ll see. We will not delude ourselves so much, “a holy place is never empty”, and new tools will appear to extort money from users, the process is endless. But with the substitution of numbers, of course, a disgrace, they cannot cope with this “super task”. But you need to cope, and in any case you have to cope. Probably, the point here is not scammers, but the fact that it is necessary to effectively close all the possibilities to replace the number, since we in Russia decided to use the number as the identifier of a specific person. Here, rather, it is politics at the state level, and all these battles with scammers are more simply an excuse and a by-product. But I must admit that the by-product turned out to be good and more than worthy of praise.

For what and with what we pay, “MTS Bank” shares numbers

MTS Bank has studied how the preferences of Russians have changed when paying for goods and services using plastic cards and mobile contactless payment – pay-services. Analysis of our own data from October 1 to November 30, 2020 compared to the same periods in 2019 and 2018 showed that for the current year the share of mobile services in the total money turnover of card transactions increased to 23%, and the share of transactions – up to 25%.

The 2020 pandemic has spurred the growth in the popularity of contactless payments in offline stores and online payments on the Internet. In March 2020, during an outbreak of coronavirus infection, the Bank of Russia recommended that residents of the country avoid using cash and pay for goods and services contactlessly. The rise in popularity of pay-services was also facilitated by the appearance of such a payment function on many sites and in mobile applications.

“The share of pay-services in the total money turnover of card transactions increased in October-November 2020 to 23% from 18% a year earlier, and the share of transactions – up to 25% from 21%, respectively. Russians still prefer to pay with a smartphone more often: on average 25 payments per month versus 16 from “plastic”, a year ago – 23 and 16, respectively.

Smartphone use in payments continues to grow rapidly. In October-November 2020, holders of MTS Bank cards using mobile contactless payment services paid with them at retail outlets 4,2 times more often than with “plastic”; a year earlier – 3,7 times more often. Cash turnover using mobile services increased by 54%, and the number of transactions – by 37%, while the growth in “plastic” was only 6% and 2%, respectively.

The proliferation of smartphones with NFC support in Russia also directly affects the growth in the popularity of payments using mobile contactless payment services. According to the MTS retail network, the share of sales of NFC smartphones in January-November 2020/2019 increased to 61% from 51% of the total number of smartphones sold.

In October-November 2020, Apple Pay was still the most popular service among MTS Bank clients, but its share is significantly decreasing every year. Apple Pay was used for 39% of transactions, Google Pay – 35%, Samsung Pay – 23% and only 3% – the rest of the pay-services. For comparison, in the same period last year, Apple Pay accounted for 49%, Google Pay – 31% and Samsung Pay – 20% of transactions. A year earlier, Apple Pay accounted for more than half of all payments – 53%. The decline in the share of Apple Pay is due to the decline in Russians’ interest in the iPhone, sales of which, according to MTS, in the first nine months of 2020 are only 10% and rank fourth after smartphones Samsung, Honor and Xiaomi.

The most popular payments among Russians, just like a year ago, are purchases in supermarkets and grocery stores, as well as payments in cafes and restaurants. In October-November 2020, 58% of transactions from smartphones and 50% from “plastic” were made in these categories. A year earlier, these figures were 63% and 54%. The decline in the share was influenced by a significant reduction in spending in public catering.

The most significant growth in the popularity of contactless payment services was shown by such categories as telecommunications services – 2,2 times, household goods – 2,1 times and car service – 2 times compared to last year.

Do Apple users themselves know that they have lost interest in Apple?

Here, I’m still interested in the phenomenon of the declared decline in Russian interest both in Apple products and, accordingly, in Apple Pay. At least this is hinted at by the figures cited by MTS analysts. It seems to me that the point here is not a drop in interest in Apple, but in a relatively sharp increase in interest in other payment services, which “skews” the statistics. Actually, the same can be assumed with regard to iPhone smartphones, the demand for them is stable and seems to be growing smoothly (I do not follow closely), but at the same time it seems to be falling against the background of rapidly growing demand for other models. It is appropriate to recall here that Apple Pay has been operating for a long time and market saturation has already passed the stage of explosive growth. Also, percentages are always apt to be misleading because of their relativity. Roughly speaking, if a small workshop assembled two cars a day, and suddenly began to assemble four cars, then this is a twofold increase in productivity, wow! And if he collected three, then freshly assembled four cars are also good progress, but nothing sensational. And if he always collected and continues to collect three cars – this is a disaster and deep stagnation, the shop is clearly on the verge of bankruptcy. This is especially noticeable against the background of competitors from the neighboring workshop, who had never assembled cars at all before, but then, looking at their colleagues, they decided to join this business, strained themselves and also assembled as many as three cars in a month. Their productivity growth at zero point of reference is generally off scale, right? It is more correct to look at absolute figures and compare the dynamics of the percentage of service users within the ecosystem, but for some reason we like to dump everything into one common heap.

Probably, in the end, everything will more or less settle down and the “crafty” percentages will begin to correspond to the average market dynamics of payment services development. In the meantime, we use what we are given, or we ourselves extract scarcely published absolute figures and calculate percentages, or we extract reports from analytical companies that are professionally engaged in this activity. The last way is the most effective, but for complete reports they usually ask for a lot of money, and such reports are more interesting to other professionals. Not to mention the fact that even with the sale of such a report, the absence of a transfer of rights to publish is probably stipulated.

Related Links

Share:

we are in social networks:

Anything to add ?! Write … eldar@mobile-review.com