Hey.

Summing up the results of 2020, in one of the materials he mentioned that deficit has become a key word for the market, it was difficult or even impossible to get components. The controversy after this material unfolded in the mail and in closed groups, the topic is close to those who produce or buy electronics.

It was surprising to me that many market participants sincerely believed in the best and that the situation would return to normal in the coming months, and some even claimed that this would happen in January. My opinion has not changed, the shortage will remain a key phenomenon in 2021 for most of the electronics, which will affect the cost of devices, and for some manufacturers – and the quality.

As an indirect, albeit anecdotal confirmation, one can look at car manufacturers. We read the Wall Street Journal, the newspaper writes that Fiat Chrysler has temporarily closed car factories in Brampton (Ontario) and a factory producing small SUVs in Mexican Toluca. Ford stopped the work of its Louisville, Kentucky plant for a week from Monday, and Toyota cut production by 40% in Texas in January. Exactly the same approach in Europe and Asia, the same Volkswagen (brands VW, Skoda, Seat, Audi) has cut production since December. In all cases, missing electronics is to blame; large automakers cannot procure components.

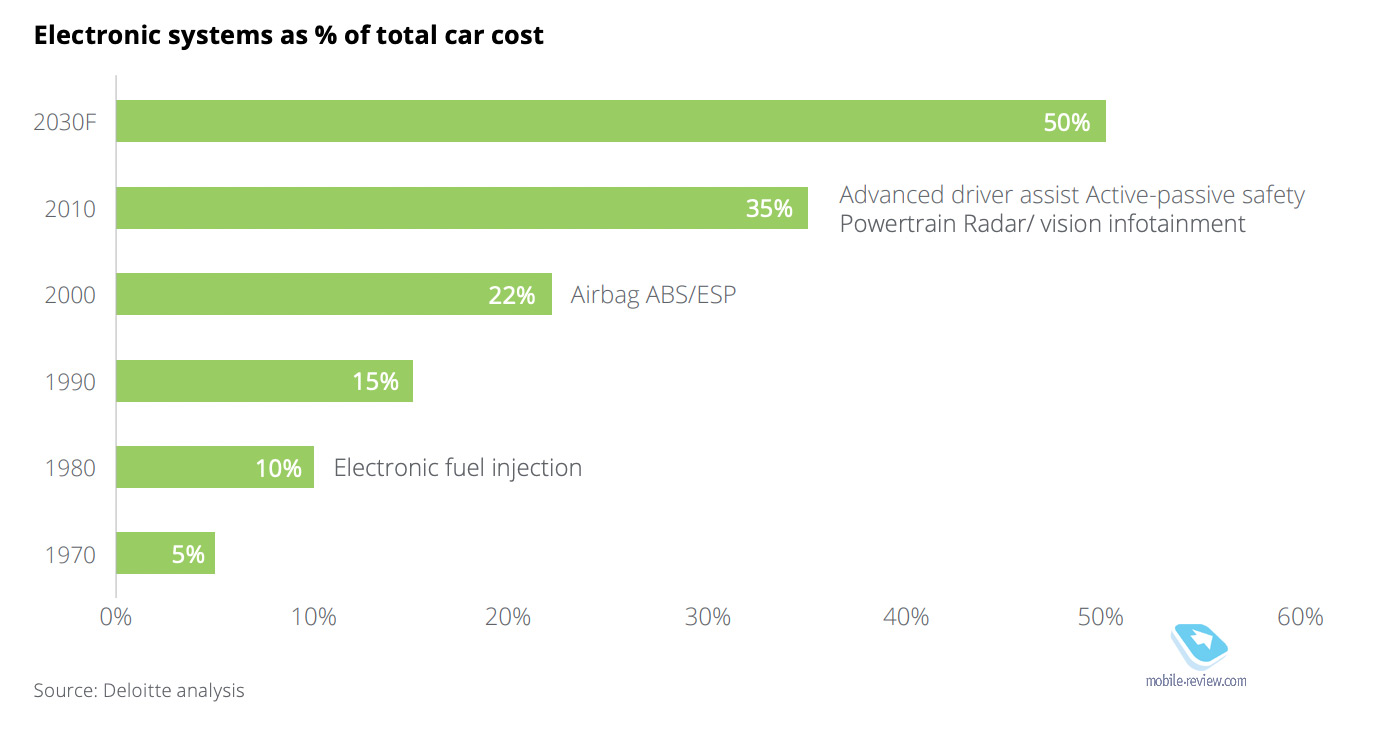

It still seems to people that machines are not yet fully equipped with electronics, they have little idea of the influence of components on the production of these “glands”. What do you think is the percentage of electronics in the cost of a modern car? In 2020, it was about 40% for all cars on the market. By 2030, electronics will take up half the cost of a car.

Notice how certain technologies penetrated machines, their development went very fast.

For those interested in semiconductor development and new niches, including AI computing and hardware, I recommend the Deloitte report, it is quite curious and outlines the direction in which the market is developing.

The pandemic has changed the entire market, but first of all, let’s look at the cost of logistics, delivery of goods from point A to point B. Historically, the fastest way to deliver goods is by plane, it is the most expensive and unacceptable for many goods, the cost of logistics is too high. Container transportation by sea from South-East Asia, in particular, China, is an affordable, easy and cheap way. But due to measures to limit the epidemic, the cost of services has grown significantly, and this applies to both international transport and local in the region of one region / country. In 2021, logistics becomes the seller’s market, not the buyer’s, as there are not enough people, containers, and free slots. Economic activity in the world has fallen, but not as expected, but transportation has changed a lot in type, direction, seasonality for many goods has gone. In electronics, the cost of logistics was rarely more than 2-3% of the price of a device, including a budget one (for flagships it is even less, although higher in absolute numbers). The price of logistics today has grown significantly, the worst is for budget devices, as well as large household appliances that take up volume. And it can be argued that only a change in the price of logistics can lead to an increase in retail prices worldwide if the goods are not produced locally. For example, a popular C-brand in December 2020 was selling a home vacuum cleaner for 3 rubles in Russia, the price on store shelves. The cost of logistics in the prime cost was about 000 rubles, delivery by sea. Since 240, the terms have increased, and the cost starts from 2021 rubles. This is just one example of how the logistics price for one product changes, but there can be many more such examples.

Logistics is killing the budget segment, any goods that take up space and weight. For many countries, the urgent question arose of resuming local production, since it is more profitable than importing goods from other countries. To some extent, the trouble helps to recreate local production, we will see a kind of renaissance of such factories. The story should not be expected to develop exponentially, since, in addition to logistics, there is another limitation – a shortage of components.

When everything is so bad that it is delicious in the moment

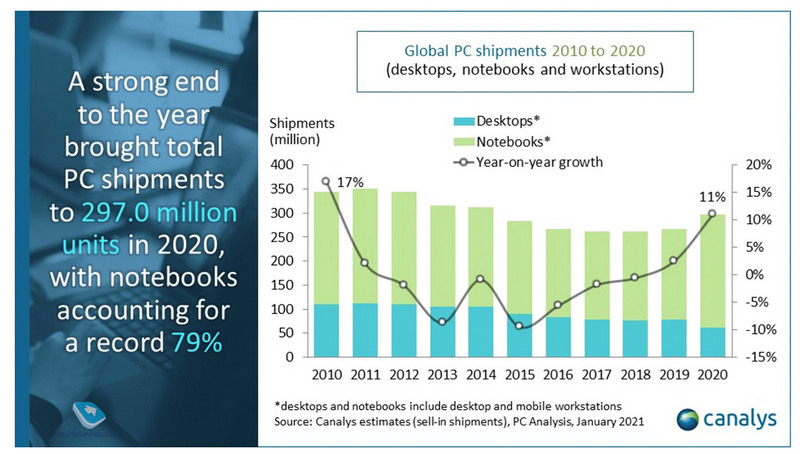

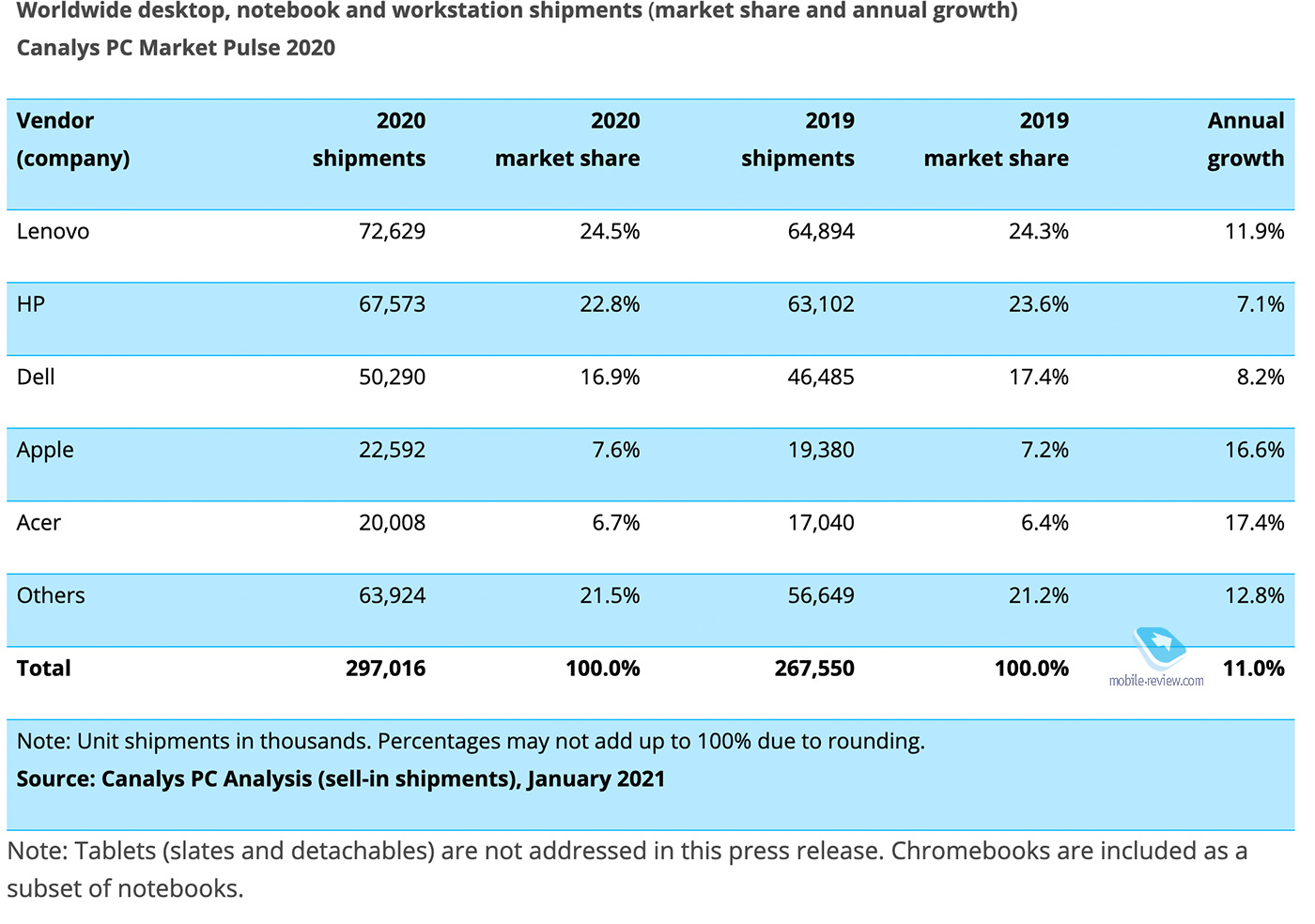

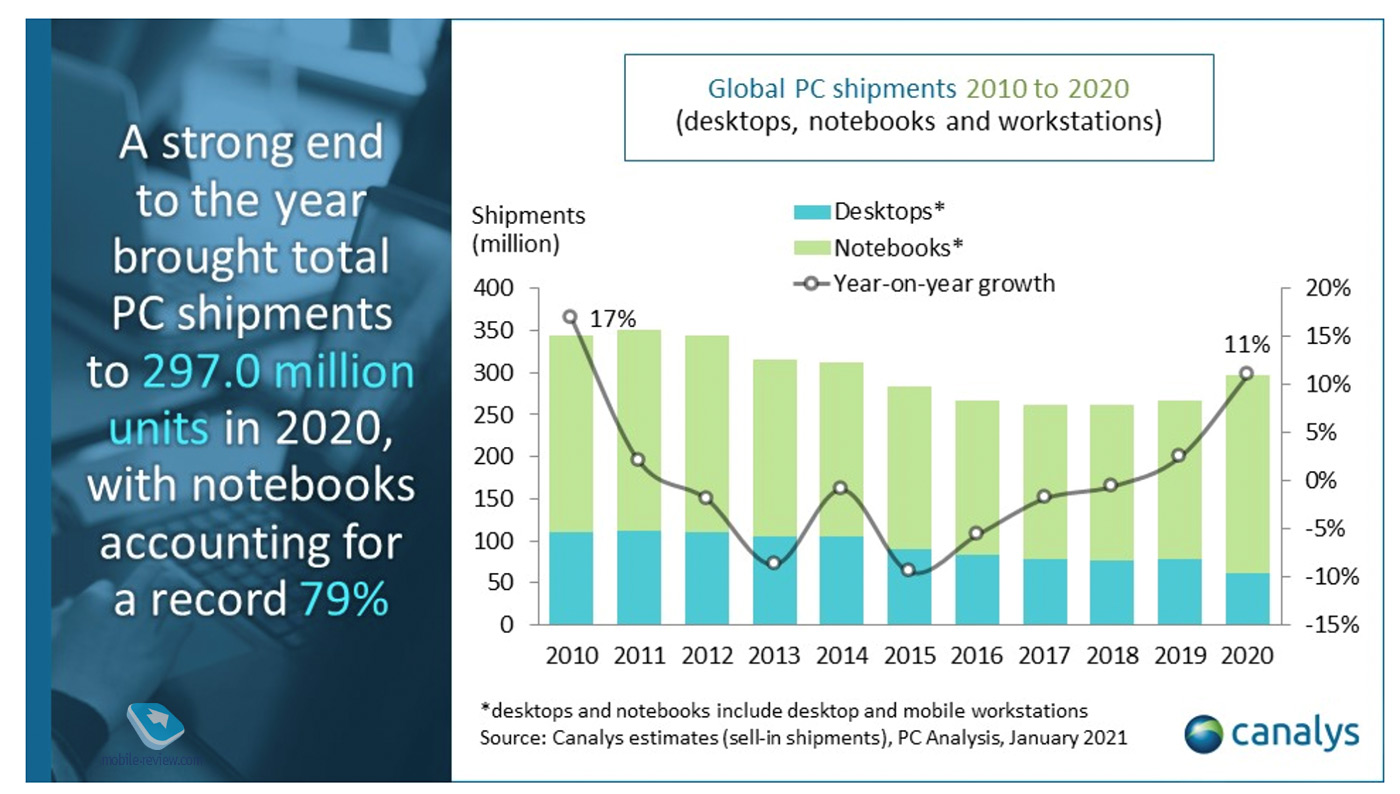

The shortage is perfectly illustrated by the sale of computers in 2020, both laptops and stationary PCs. Look at the sales data.

11% YoY sales growth, which doesn’t seem like a big deal, right? But if you look at the laptop category, and also take into account that the growth was in developed countries, and not in the third world, then the picture is completely different.

Since 2011, the PC market has been constantly sagging, and the current takeoff was not foreseen by any forecast, it is anomalous. This deficit characterizes the fact that supply and demand are distributed unevenly. As a consequence, retailers and manufacturers are transferring goods from one market to another. For example, many laptop vendors pick them up from warehouses in Eastern Europe and move them to Russia or Western Europe where demand is higher. The top-level picture of the world does not give an idea of the local nature of the deficit; it follows from the situation in specific countries. But on the example of Russia it is good to illustrate the local nature of the deficit and the lack of goods on the shelves.

For example, let’s take into account the iPhone 12 Pro / Pro Max, which are not being produced in sufficient quantities because Apple cannot get the required components. These models enter the Russian market in insufficient quantities, they are replaced with old devices that are available. The likelihood of selling such expensive models is higher in Moscow and large cities, so logistics delivers them in this order, the priorities are just that. This increases the turnover of goods, removes waiting times for buyers. Before the New Year, my friend could not buy several iPhones in Tyumen, which he planned to present for the holiday. The reason is exactly the same distribution by city, the likelihood that they will be sold in such and such colors and configurations was small, so retail players did not import them. And in fact, we are stuck with the fact that these devices are needed to order. Is there a shortage of iPhone 12 Pro in Tyumen? Definitely yes. But this is a shortage, characterized by the moment, one cannot buy these devices here and now. As soon as one of the retail players delivers more iPhones to this region, sales will stop, as there is no constant, stable demand.

On the example of the iPhone, we see two factors: the first is insufficient supplies to the country, and the second consequence follows from it, it is impossible to provide store shelves in all regions so that the goods lie and wait for their customers. Roughly the same situation occurs all over the world, which forces manufacturers to transfer goods from one market to another. Habitual planning, which existed before, flew to hell.

The shortage of laptops forces people to look for a substitute product, tablets are perfect for its role, fish for fishlessness and cancer. Therefore, tablet sales in 2020 have also grown strongly, but will this factor continue in 2021? I’m sure not. The main expenses on preparation for isolation fell on 2020, and now we are raking the consequences of the global deficit and the lack of the usual logistics. Previous crises teach us that it usually takes 1.5-2 years, there is no reason to believe that this time everything will work out faster.

In Russia, it is clearly seen how the deficit is formed, how customer expectations are changing. People are not ready to buy the bulk of the goods that they are not satisfied with, they want to get a specific product for their money. For example, if they are guided by the purchase of a smartphone from Xiaomi for 30 thousand rubles, then it will be difficult to convince them to buy Samsung, Huawei or something else. Five years ago it was much easier to reorient the customer to another brand. And here we come to the fact that deferred demand is forming, it also determines the formation of a deficit. Running, popular models are waiting, while they do not buy those devices that are not interesting. The paradox of this phenomenon is that there is an imbalance, there are brands and models of electronics that have the maximum turnover, and there are goods that are sold very badly and pull the retail economy down. Assortment management is coming to the fore for all players in the world. The same example from Apple shows that the lack of adequate planning does not allow the iPhone 12 Pro / Pro Max to be produced in sufficient quantities, the company is forced to shift the focus to older models. The deficit is not global, in which subsequent demand is guaranteed. And this explains why Apple does not run to order components at any cost, for the company it makes no sense. By purchasing the components at a higher price, Apple will be faced with the fact that they cannot sell the entire product. And local deficit is more profitable for the company than full satisfaction of demand. Exactly the same situation with car manufacturers, the absence of components makes it possible to form deferred demand, the main thing is that the situation is the same for all major players, without exception.

For buyers in this story, there is not much positive, prices for many product groups are growing (older models do not receive noticeable discounts). But, as always, this process is uneven, for some manufacturers this is so, for others it is not at all. For example, large companies hardly change their pricing strategy, there are discounts, interesting offers and an attempt to capture a large market share. But small companies have a hard time, as prices for their products are growing 1.5-2 times on store shelves and they have to switch to survival mode. And if earlier small electronics manufacturers differed from A-brands in cost, today this factor is no longer there.

As a conclusion, we can say that the time is not the best for C-brands. Prices for their products are growing, demand is naturally decreasing (people want to buy well-known brands, since in their eyes this means quality and a long service life, the crisis mode in the minds of consumers works like this). For A-brands that have resources and a vertical structure, everything is fine, they are insured against a lack of components, they can produce sufficient quantities of goods and capture market share. For those who focus on contract manufacturing, the situation is individual in each case, here you need to look at each story separately.

The paradox of the 2021 deficit is that it exists and allows companies to explain the rise in prices. On the other hand, this factor should not be overestimated, since it is often only a way to increase your income, and not a reaction to a real imbalance in the market. The crisis has not gone anywhere, so sales in each segment will decline, while food prices will rise. This has always been the case, and this crisis is no exception, despite the fact that money is printed in most countries of the world. Although this is more likely due to this, since the inflation process in 2020 was launched, but it has not yet been taken into account in the cost of electronics, the revaluation will affect us in mid-2021.

Related Links

Share:

we are in social networks:

Anything to add ?! Write … eldar@mobile-review.com